GBI Shifts to Second Straight Month of Slowing Contraction

While contraction has been an ongoing course for activity in the GBI: Moldmaking, its slight slowing might suggest that positive change is coming.

#ecomonics

Share

GBI: Moldmaking activity was up a point in October. Photo credit, all images: Gardner Intelligence

Moldmaking activity contracted for a seventh month in October, though at a slower pace, so that the index appears more in line with what was seen in July. The Gardner Business Index (GBI) Moldmaking, ended the month at 45.5, almost fully recovering the second of two points lost in August.

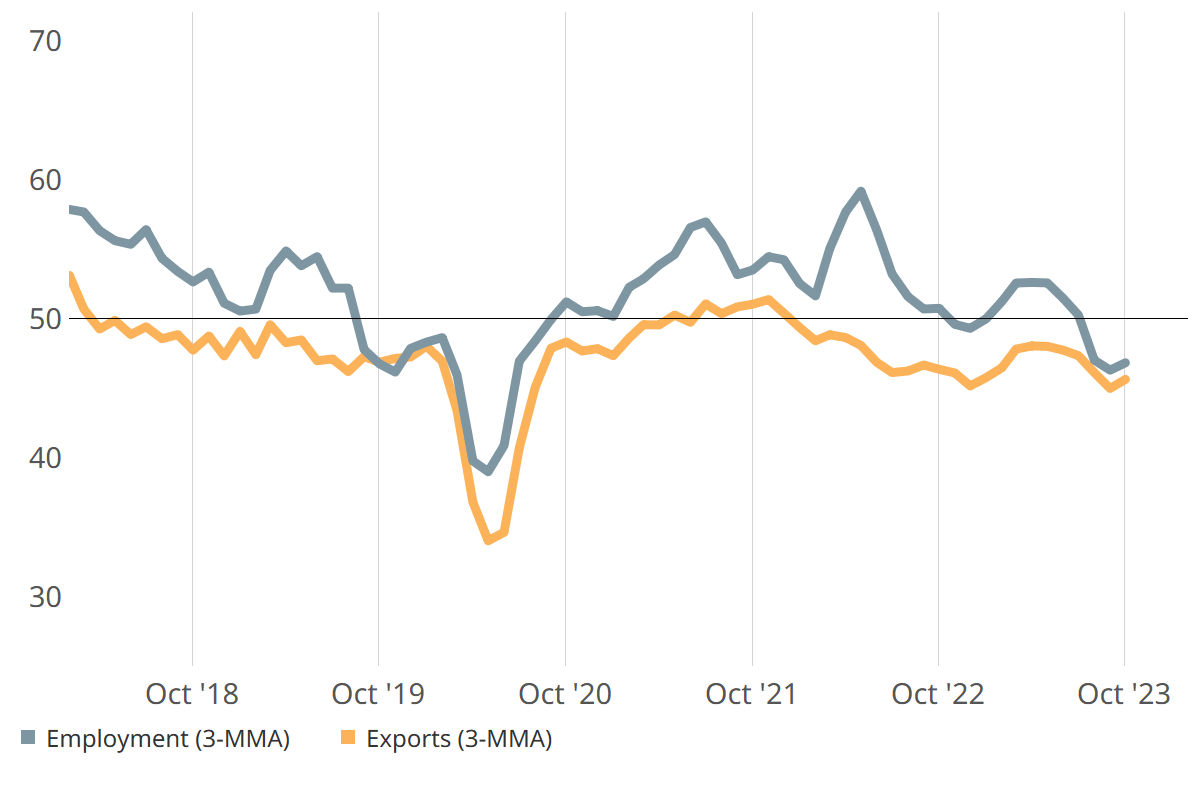

All components contracted again, though some stabilized or slightly slowed the rate of their contraction. Overall, activity here saw a little bit of everything — movement in every direction, that is — in October. Employment, after significant accelerated contraction in August, contracted a bit more slowly here. Exports, which have paralleled employment for about a year, behaved similarly, albeit at a deeper level of contraction. Production and new orders leveled off in October, though, like all other components, continues to contract as well. Supplier deliveries continued along its new path in contraction territory, while backlog accelerated along its established path of contraction, landing as the lowest component in the moldmaking index.

Employment and exports followed similar paths of contraction, slowing a bit in October. (This graph is on a three-month moving average.)

RELATED CONTENT

-

New Orders, Production Register Slowing April Activity

Total new orders for April registered slowing growth while export orders contracted. Much of the expansion in moldmaking orders during COVID-19 has come from domestic demand.

-

Moldmaking Industry Ends Four-Month Expansionary Run

Slowing new orders, production and backlog activity result in a 47.9 reading for November, indicating a potential incoming challenge for the world supply chains as we enter 2021.

-

Moldmaking Industry Accelerates Into 2022

Moldmakers have learned to do more with less, according to January Index readings. Production activity has remained robust, despite a relatively weak employment market and struggling supply chains.